Employees’ Provident Fund of Malaysia (EPF) plays a central role in securing Malaysians’ retirement needs. As Malaysia’s public provident fund, EPF serves over 14.5 million members and manages a portfolio value of over RM1.0 trillion.

With digital channels becoming a norm in work and lifestyle needs, the importance of building these channels must be a priority. To that end, EPF has recognised these growing demands and initiated its Operations Transformation 2.0 back in 2017. Since then, the fund has engaged in several digitalisation initiatives. These initiatives serve to improve both the customer experience and internal operational efficiency.

Our article seeks answers to the following questions:

- How is EPF improving the digital experience of its members?

- How is EPF creating new channels & services to drive the participation of its members and widen its coverage?

- What are the solutions adopted by EPF to support its digital infrastructure?

Building a comprehensive omnichannel experience

- Continuous enhancement to the i-Akaun platform on mobile and web applications

The i-Akaun platform is the primary digital channel for a customer’s interaction with EPF. It is accessible via the internet and more recent mobile applications – the i-Akaun app (for members) and the e-Caruman app (for employers). Some functions performed through these applications include checking account balances, monitoring transaction status, enabling payments, etc.

Since its launch, EPF has continuously introduced new updates/services onto its i-Akaun mobile application. In 2019, several updates included new PDF-Format statements for downloads, targeted push notifications, a branch location service, and fund performance monitoring for its i-Invest users.

With these improvements, the i-Akaun platform has gained commendable acceptance among its members in the past five years. From 2017, the growth in i-Akaun membership grew by at least 70%, with 52.06% of their 14.5 million members registered on i-Akaun. On the employers’ side, 99.36% of 522,297 employers registered for i-Akauns.

To date, the i-Akaun application has nearly 1.5 million downloads with an average rating of 4.5. Both the growing user base and reviews reflect EPF’s focus on building these digital channels.

- Enhancements to brick-and-mortar branches

To extend the digital experience onto its physical branches, EPF has continuously introduced new processes to improve customer interactions at the branch. The focus here is to provide effective self-service channels and superior customer service.

EPF designed its branches as a with a one-stop-centre approach. Apart from e-kiosks, EPF also introduced initiatives to provide advisory training for its staff. Customers today, however, tend to prefer self-service channels due to their efficiency and ease of use. Hence, EPF recognised that its staff could provide higher value as retirement advisors.

To execute this training plan, EPF introduced the Retirement Advisory Services (RAS) in July 2014, which is now available in 52 branches. The latest figures show that more than 82,000 members received advisory services that RAS provided.

- E-payroll Services for SMEs

EPF also pays attention to services beyond its core functions. For example, in June 2021, EPF unveiled an e-Payroll service to assist small business owners and entrepreneurs with a digitalised payroll system. This service complements the i-Akaun platform for employers. It ensures that they meet and monitor statutory obligations and employee contributions.

The e-payroll service aims to ease the difficulties small business owners face in terms of the financial constraints to adopt a digital payroll solution. Some features include the ability to store digital records, monitor account contributions, automate calculations, etc.

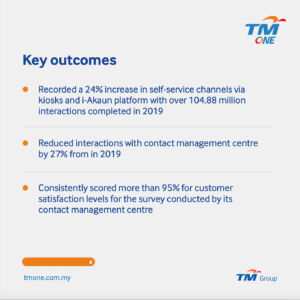

The range of services provided by EPF is indeed commendable. The increase of customer interactions through electronic channels suggests that customers are strongly shifting towards digital channels provided by the fund. In 2019, self-service channels via kiosks and the i-Akaun platform recorded 104.88 million interactions, a 24.12% increase from 2018.

EPF’s Contact Management Centre (CMC), which handles customer inquiries mainly through telephone or email, recorded a 27.16% decrease from 2018. Customers are increasingly attuned to digital channels as opposed to traditional face-to-face interactions according to these statistics.

Launched new services to drive participation & increase coverage

- Introduced i-Invest platform to drive participation from members

One of the recent highlights from EPF was the introduction of i-Invest in 2019 on its i-Akaun platform. This service allows EPF members to invest part of their Account 1 savings into EPF-approved unit trust funds.

The introduction of this service was a new one for the industry. EPF was the first public retirement fund that allowed its members to invest their retirement savings directly into unit trust funds of their choice. Customers also enjoy significantly lower sales charges through this service. The sales charge ranges from 0%-0.5%compared to the standard range of 2%-3% often charged by intermediaries.

The i-Invest service also includes tools for its members to monitor relevant information on the unit trust funds they selected actively. Through these tools, EPF encourages higher participation from its members.

- Building programs for gig economy workers

EPF continues to face the challenge to cover a broader range of Malaysian workers. The growing size of the gig economy is one of the leading causes for this. Estimates indicate that gig workers would represent more than a third of Malaysia’s labour force in the next five years. With the pandemic’s impact on job losses, this situation may worsen as Malaysians continue to find alternative income sources.

To counter this, EPF introduced the i-Saraan programme in mid-2020. Through this programme, self-employed workers can voluntarily contribute to their EPF accounts. This program was designed to encourage gig economy workers to save up for retirement. The pickup has been encouraging, with recent registrations increasing by 22.11% in 2019 with 120,738 registrations.

The government has also championed this initiative by introducing a RM50million matching grant for i-Saraan investors in June 2020. Moreover, EPF has engaged with the private sector, most notably collaborating with Grab Malaysia by extending their MOU that was signed back in 2018. Like the government’s matching grant, this MOU commits Grab to match contributions by up to 5% with a ceiling of RM80 annually for those below 55 years old. Those above 55 years old are guaranteed matching contributions of 10% with a ceiling of RM120 annually.

How you can emulate EPF

- The customer satisfaction levels are a reflection of the customer-focused culture that is present in EPF. Merely digitalising is not the answer. Businesses need to understand the specific customer journey pain points to build solutions effectively.

- Observing EPF, the fund placed strong emphasis on creating a comprehensive omnichannel experience, one that could meet the demands of different types of customers. This is crucial to ensure consistent customer satisfaction and provide a seamless onboarding process onto digital channels.