This is the era of “the platform economy”. Seven of the world’s top 10 companies based on market capitalisation are platform companies. Open innovation is a business model construct that enables these companies to grow rapidly at a massive scale and speed. They are able to take advantage of all sources of creativity through partnerships with companies and individuals alike. Open Banking is about bringing this capability of open innovation to the banking and financial services industry. Regulators around the world recognise the tremendous potential of this new business model and are facilitating the move towards enabling the banks to collaborate and innovate.

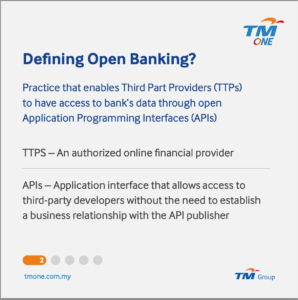

Defining Open Banking

Open banking is simply the practice of enabling Third Party Providers (TPPs) to have access to banks’ data through open Application Programming Interfaces (APIs).

Application Programming Interfaces (APIs):

- Broadly categorised into private, partner, and open APIs

- Open API is an application interface that allows access to third-party developers without the need to establish a business relationship with the API publisher

Third-Party Providers (TPPs):

- An Authorised online financial service provider

- There are two types of TPPs:

- Account Information Service Provider (AISP)

Authorised access to account data provided by financial institutions and banks

- Payment Initiation Service Provider (PISP)

Authorised access to initiative payments in and out of a user’s account

- Account Information Service Provider (AISP)

What can you expect as a consumer?

The explosive innovation possibilities pave the way for great consumer experiences. The specific benefits for consumers include:

- Ownership of your data: Consumers will now be in control of their data. They can share their financial data from one bank with another. They can have a consolidated view of their financials across multiple banks in one place. They will be able to share their data with third–party providers in a frictionless manner.

- Unprecedented choice and innovative services: Consumers will now have access to a whole plethora of innovative services from fintechs and third parties. These companies will be able to leverage off the core banking infrastructure of the established banks to offer these new services. As a consumer, you will have access to the best of both worlds, viz., the security and trust provided by your traditional bank; and the innovation of new start-ups.

- Frictionless consumption of services: This will be the biggest change by the end of the decade. We will likely consume more financial services on third-party websites than on banks websites. It will drive an era of invisible banking.

Benefits for Banks

.

Many banks worry that Open Banking will unleash a new wave of competitive intensity caused by the entry of new market participants. Nonetheless, the benefits far outweigh the challenges. The opportunity for growth is immense and the banks will emerge as the biggest beneficiaries of this new ecosystem approach. The benefits for the banks include:

- Improve overall consumption of financial services: The traditional closed–door approach to innovation has limited the overall per capita consumption of financial services. The high degree of funding available to fintech start-ups is ushering in a new wave of innovative products. The banks can now partner, collaborate, and offer all of these services via their platforms. Open Banking will drive an unprecedented increase in the per capita consumption of financial services.

- New business model: Consumers trust banks with their money and data as compared to fintech and tech-giants. As the principal owners of the consumer trust, they have this opportunity to be the aggregator and the owner of the consumer experience. This will enable them to transition to drive revenues from new streams such as Data monetisation and Ecosystems.

The stage is set in Malaysia for Open Banking

In June 2016, Malaysia’s central bank and principal financial services regulator, Bank Negara Malaysia (BNM), established a Financial Technology Enabler Group (FTEG)[1] to support innovations within the BFSI sector. The FTEG plays the role of developing new policies and enhancing existing ones related to the adoption of new technologies in the sector.

Consequently, in 2017, FTEG launched a FinTech Regulatory Sandbox framework to test new and applicable technology, including Open Banking.

In March 2018, BNM made their biggest stride yet by establishing an Open API Implementation Group. This was to develop standards and regulations around open data, security, oversight arrangements for TPP, and rights of access. The group was also accountable to review the existing regulations regarding controls on customer information.

As of 2021, BNM is taking a phased approach towards Open Banking; they are cognizant of the security threats and governance measures that would need to come along with it. The central bank is also welcoming additional proposals from the BFSI, FinTech community, and any interested parties that would benefit from standardised open APIs.

The future

The UK and the Nordics in Europe are at the forefront of building a world-class Open Banking digital ecosystem. These countries have their framework and API standards in place to facilitate the process. They also have a vast digital infrastructure that enables the widespread use of Open Banking.

The global and regional acceleration of Open Banking will be a catalyst towards Open Banking in Malaysia. With the right governance, regulations, and security checks in place, Malaysia will soon follow suit with these leading countries in implementing Open Banking. With the most digital natives in SEA[2] (83% adoption of digital customers*) and a vibrant fintech ecosystem, we certainly have the right ecosystem in place to make this happen.

[1] Publishing Open Data using Open API. (2019).

[2] Devanesan, J. (2020). Malaysia has the most digital natives in South East Asia – Tech Wire Asia

Read Now